Different Types of Trusts for Seniors

March 4, 2025

Discover the secrets of senior financial planning with different types of trusts. Safeguard your future with the right trust for you!

Understanding Trusts for Senior Financial Planning

When it comes to senior financial planning, trusts play a crucial role in ensuring the protection and management of assets. Trusts are legal arrangements that allow individuals to transfer their assets to a trustee who holds and manages them on behalf of beneficiaries. They offer various benefits, including asset protection, estate planning, and tax advantages. Let's delve into the importance of trusts in senior financial planning and provide an overview of different types of trusts.

Importance of Trusts in Senior Financial Planning

Trusts are particularly important for seniors when it comes to safeguarding their assets and securing their financial future. Here are a few reasons why trusts are essential in senior financial planning:

- Asset Protection: Trusts provide a level of protection for seniors' assets against creditors, lawsuits, and potential financial exploitation. By placing assets in a trust, seniors can ensure their wealth is preserved for their own use and for the benefit of their loved ones.

- Estate Planning: Trusts serve as a valuable tool in estate planning for seniors. They allow individuals to outline their wishes regarding the distribution of assets after their passing. Through trusts, seniors can ensure that their assets are distributed according to their specific instructions, minimizing the potential for disputes among beneficiaries.

- Probate Avoidance: Trusts can help seniors avoid the probate process, which can be time-consuming and costly. By transferring assets to a trust, seniors can ensure a smoother and more efficient transfer of their assets to their beneficiaries after their passing.

- Continued Financial Management: Trusts provide a mechanism for seniors to maintain control and management of their assets even if they become incapacitated. By appointing a trustee, seniors can ensure that their financial affairs are handled according to their wishes, providing peace of mind during challenging times.

Overview of Different Types of Trusts

There are several types of trusts available for senior financial planning, each with its own unique characteristics and purposes. Here is a brief overview of the different types of trusts commonly used:

Understanding the importance of trusts in senior financial planning and being familiar with the different types of trusts available can empower seniors to make informed decisions about their assets and estate plans. It's recommended to consult with a qualified estate planning attorney or financial advisor to determine the most suitable trust options based on individual circumstances and goals.

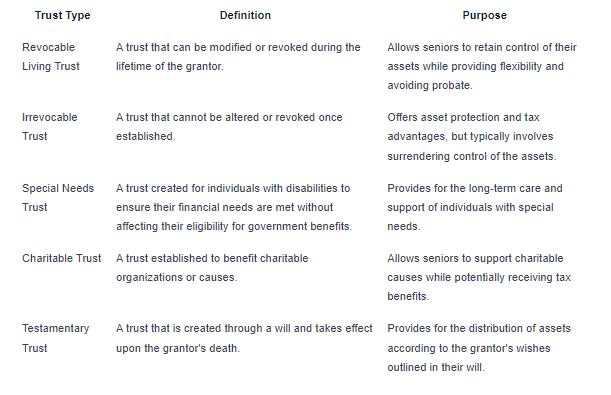

Revocable Living Trust

A revocable living trust is a popular option when it comes to senior financial planning. This type of trust provides flexibility and control over assets while allowing for seamless estate planning. Let's delve into the definition, purpose, as well as the benefits and considerations of a revocable living trust.

Definition and Purpose

A revocable living trust is a legal arrangement in which an individual, known as the grantor, transfers their assets into a trust during their lifetime. The grantor can modify, amend, or revoke the trust as long as they are mentally competent. Upon the grantor's passing, the trust assets are distributed to the beneficiaries according to the instructions outlined in the trust document.

The primary purpose of a revocable living trust is to avoid probate, which is the legal process of distributing assets after a person's death. By placing assets in a trust, they are no longer considered part of the grantor's probate estate. This can help streamline the transfer of assets to beneficiaries and potentially minimize costs and delays associated with probate.

Benefits and Considerations

Revocable living trusts offer several benefits for seniors in their financial planning:

- Probate Avoidance: One of the key advantages of a revocable living trust is the ability to bypass probate, which can be time-consuming and costly. By transferring assets to a trust, the grantor ensures a smoother transition of assets to beneficiaries upon their passing.

- Privacy: Unlike a will, which becomes a public record upon probate, a revocable living trust allows for the privacy of the grantor's estate distribution. This can be advantageous for individuals who prefer to keep their financial affairs confidential.

- Flexibility: The grantor retains the ability to modify or revoke the trust during their lifetime, providing flexibility to adapt to changing circumstances. This can include adding or removing assets, changing beneficiaries, or amending distribution instructions.

- Incapacity Planning: A revocable living trust offers provisions for incapacity planning. In the event that the grantor becomes mentally or physically incapacitated, a successor trustee can step in to manage the trust assets on their behalf, ensuring continuity and avoiding the need for court-appointed guardianship.

Despite the benefits, there are considerations to keep in mind when establishing a revocable living trust:

- Cost: Setting up a revocable living trust typically involves legal fees. However, the potential savings in probate costs and time may outweigh the initial expense.

- Funding: To fully benefit from a revocable living trust, it is essential to transfer assets into the trust. Failure to fund the trust properly may result in assets being subject to probate.

- Tax Implications: While a revocable living trust does not provide direct tax advantages, it allows for effective estate tax planning. Consulting with a financial advisor or estate planning attorney is recommended to navigate potential tax considerations.

By understanding the definition, purpose, benefits, and considerations of a revocable living trust, seniors can make informed decisions when it comes to their financial planning. It is advisable to consult with a qualified professional to determine if a revocable living trust aligns with specific needs and goals.

Irrevocable Trust

An irrevocable trust is a type of trust that, once established, cannot be modified or revoked by the grantor (the person who creates the trust). This means that once assets are transferred into the trust, they are no longer under the direct control of the grantor. Irrevocable trusts are commonly used in senior financial planning for various purposes.

Definition and Purpose

The primary purpose of an irrevocable trust is to protect and manage assets for the benefit of the beneficiaries. By transferring assets into the trust, the grantor effectively removes them from their estate, potentially reducing estate taxes and protecting the assets from creditors.

Unlike a revocable living trust, which allows the grantor to retain control and ownership of the assets, an irrevocable trust places the assets outside of the grantor's estate. This can be particularly advantageous for seniors who want to ensure the preservation of their assets and their ability to qualify for government benefits, such as Medicaid.

Benefits and Considerations

Irrevocable trusts offer several benefits in senior financial planning. Let's take a look at some of the key advantages and considerations:

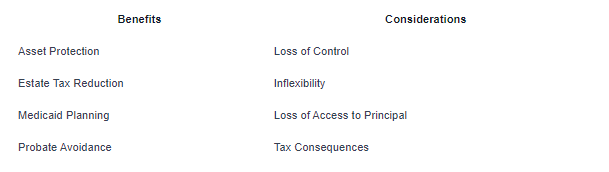

Asset Protection: By placing assets in an irrevocable trust, seniors can protect those assets from potential creditors. This can be especially valuable for individuals who want to safeguard their wealth for future generations.

Estate Tax Reduction: Irrevocable trusts can help reduce estate taxes by removing assets from the grantor's taxable estate. This can be particularly important for seniors with large estates who want to minimize the tax burden on their beneficiaries.

Medicaid Planning: Irrevocable trusts can be used as part of Medicaid planning strategies. By transferring assets into an irrevocable trust, seniors may be able to qualify for Medicaid benefits while preserving their assets for their loved ones.

Probate Avoidance: Assets held in an irrevocable trust generally pass outside of probate, allowing for a smoother and more efficient transfer of assets to beneficiaries upon the grantor's passing.

While irrevocable trusts offer various benefits, it's important to consider the limitations and potential drawbacks. One significant consideration is the loss of control over the assets placed in the trust. Once assets are transferred, the grantor no longer has the ability to modify or revoke the trust without the consent of the beneficiaries or a court order. Additionally, the inflexibility of irrevocable trusts may limit the grantor's access to the principal or income generated by the trust.

Before establishing an irrevocable trust, it is recommended to consult with an estate planning attorney or financial advisor who can provide personalized guidance based on your specific circumstances and goals.

Special Needs Trust

A special needs trust is a type of trust specifically designed to provide financial support and security for individuals with special needs or disabilities. It is an essential tool in senior financial planning when the senior has a loved one who requires ongoing care and assistance due to their special needs.

Definition and Purpose

A special needs trust, also known as a supplemental needs trust, is a legal arrangement that allows funds to be set aside for the benefit of a person with special needs without jeopardizing their eligibility for government benefits and assistance programs. The primary purpose of a special needs trust is to enhance the quality of life for the individual with special needs by ensuring that the funds are used to supplement, rather than replace, public benefits.

By establishing a special needs trust, seniors can provide for their loved ones with special needs in a way that protects their eligibility for government benefits, such as Medicaid and Supplemental Security Income (SSI). The trust can cover various expenses not covered by these programs, including medical and dental care, rehabilitation, therapy, education, transportation, and recreational activities.

Benefits and Considerations

A special needs trust offers several benefits for both the senior and the individual with special needs. Some of the key advantages include:

- Preservation of Government Benefits: By utilizing a special needs trust, the individual with special needs can continue to receive essential government benefits while still benefiting from the additional financial support provided by the trust.

- Protection of Assets: Assets held in a special needs trust are protected from being counted as the individual's personal assets for the purpose of determining eligibility for government benefits. This ensures that the funds are available to supplement the individual's needs without affecting their eligibility for crucial assistance programs.

- Flexibility and Control: The senior can have peace of mind knowing that the funds in the special needs trust will be managed and disbursed according to their instructions. They can select a trustee who will oversee the trust and make decisions regarding the distribution of funds in a manner that aligns with the specific needs of their loved one.

- Continuity of Care: A special needs trust ensures that the individual with special needs will continue to receive the necessary care and support even after the senior's passing. This provides long-term financial security and peace of mind for both the senior and their loved one.

However, it's important to consider some considerations when establishing a special needs trust:

- Legal Assistance: Creating a special needs trust requires the expertise of an attorney experienced in elder law and special needs planning to ensure compliance with legal requirements and to maximize the benefits available.

- Proper Funding: The senior must carefully consider the amount of funding necessary to provide for their loved one's ongoing needs. Balancing the amount of funding with the preservation of government benefits is crucial to ensure the effectiveness of the trust.

- Trustee Selection: Selecting the right trustee is essential to ensure the proper management and distribution of funds. The trustee should have a strong understanding of the individual's special needs and the ability to make decisions in their best interest.

By understanding the definition, purpose, benefits, and considerations of a special needs trust, seniors can make informed decisions in their financial planning to secure the future of their loved ones with special needs.

Charitable Trust

A charitable trust is a type of trust established for philanthropic purposes. It allows individuals to support charitable organizations or causes that are close to their hearts while also providing potential tax benefits. Let's explore the definition, purpose, benefits, and considerations of charitable trusts in senior financial planning.

Definition and Purpose

A charitable trust is created when assets are transferred to a trust with the intention of benefiting charitable organizations or causes. The trust is managed by a trustee who has the responsibility of distributing the trust's assets to the designated charities. The purpose of a charitable trust is to provide ongoing support to charitable causes while potentially reducing tax liability for the grantor.

Charitable trusts can be established during a person's lifetime or through a will as part of an estate plan. They allow individuals to make a lasting impact by providing financial support to organizations that align with their philanthropic goals and values.

Benefits and Considerations

Charitable trusts offer several benefits for seniors looking to incorporate philanthropy into their financial planning.

- Tax Benefits: Contributions made to charitable trusts may be eligible for tax deductions. The grantor can potentially deduct the fair market value of the assets donated, subject to certain limitations and guidelines set by tax laws. This can help reduce the grantor's income tax liability.

- Lifetime Giving: Establishing a charitable trust during one's lifetime allows the grantor to witness the impact of their philanthropy firsthand. It provides a sense of fulfillment and the opportunity to engage with charitable organizations and causes that are meaningful to them.

- Estate Planning: Charitable trusts can be useful tools for estate planning. By including a charitable trust in their estate plan, seniors can ensure that their assets continue to support charitable causes after their passing. This allows their legacy of giving to live on.

While charitable trusts offer benefits, there are also considerations to keep in mind:

- Irrevocability: Once assets are transferred to a charitable trust, they generally cannot be retrieved or redirected for personal purposes. It's important to carefully consider the impact of this irrevocable transfer on personal financial needs and goals.

- Legal and Financial Expertise: Establishing a charitable trust requires the assistance of legal and financial professionals who specialize in estate planning. It's crucial to work with experienced professionals who can guide seniors through the process and ensure compliance with applicable laws and regulations.

- Choosing Charitable Organizations: Selecting the right charitable organizations or causes to support is an important decision. Seniors should research and evaluate charitable organizations to ensure that their values align with those of the organization and that the organization is reputable and well-managed.

By considering the definition, purpose, benefits, and considerations of charitable trusts, seniors can make informed decisions about incorporating philanthropy into their financial planning. It's advisable to consult with legal and financial professionals to navigate the complexities of establishing and managing a charitable trust effectively.

Testamentary Trust

A testamentary trust is a type of trust that is created in a person's will and takes effect upon their death. It is established to manage and distribute assets to beneficiaries according to the terms and conditions specified in the will.

Definition and Purpose

A testamentary trust is established through a legal document called a will. Unlike other types of trusts that are created during a person's lifetime, a testamentary trust becomes effective only after the individual passes away. The purpose of a testamentary trust is to ensure that the assets of the deceased are managed and distributed according to their wishes, providing for the financial well-being of their chosen beneficiaries.

Benefits and Considerations

There are several benefits to utilizing a testamentary trust in senior financial planning:

- Control over asset distribution: By establishing a testamentary trust, seniors can have peace of mind knowing that their assets will be distributed according to their specific instructions outlined in the will. They have control over who will receive the assets, when they will receive them, and under what conditions.

- Asset protection: Testamentary trusts can provide protection for assets. For example, if a beneficiary is going through a divorce or has financial difficulties, the assets held in the trust may be shielded from potential creditors or legal claims.

- Tax planning: Testamentary trusts can be structured to take advantage of tax planning strategies. By distributing assets through a trust, it may be possible to minimize estate taxes or income taxes that would otherwise be incurred.

- Flexibility: Testamentary trusts offer flexibility in terms of the distribution of assets. The creator of the trust can specify different terms for different beneficiaries, ensuring that their unique needs and circumstances are considered.

However, it is important to consider some key considerations when utilizing a testamentary trust:

- Probate process: Since a testamentary trust is created within a will, it is subject to the probate process. This means that the will must go through a legal validation process before the trust can be established and the assets can be distributed. This may result in some delays in the distribution of assets.

- Lack of privacy: The terms of a testamentary trust become public record during the probate process. This means that the details of the trust, including the assets and beneficiaries, can be accessed by the public.

- Legal assistance: Creating a testamentary trust can be complex, and it is important to seek the assistance of an experienced estate planning attorney to ensure that the trust is properly drafted and aligned with the individual's wishes.

By considering the benefits and considerations of a testamentary trust, seniors can make informed decisions regarding their financial planning and ensure that their assets are distributed in accordance with their intentions.

Sources

https://www.westernsouthern.com/retirement/what-are-the-different-types-of-trusts#:~:text=Trusts%20p

https://www.cedarhurstliving.com/senior-living-blog/different-types-of-trusts-for-seniors

Similar articles

How to Navigate Financial Options for Long-Term Care

The Role of Assistive Devices in Supporting Recovery

How to Stay Connected with Your Loved One in a Nursing Home

Understanding Long-Term vs. Short-Term Stays in Nursing Homes

Why Speech Therapy is Crucial for Patients Recovering from a Stroke

The Role of Aromatherapy in Senior Living Facilities

How Long-Term Care Facilities Ensure Comfort for Residents with Mobility Challenges

The Role of Continuing Education for Nursing Home Staff

The Role of Preventative Healthcare in Long-Term Care Facilities

How Physical Therapy Supports Recovery in Short-Term Rehab

How to Develop Strength Through Resistance Exercises

How to Improve Flexibility with Physical Therapy

How Family Therapy Can Support Recovery Efforts

How to Handle Conflict Resolution in a Nursing Home Setting

The Importance of Nutrition in Short-Term Rehabilitation Recovery

How to Maintain Mobility During Short-Term Rehabilitation

The Benefits of Hydrotherapy in Rehabilitation Programs

What to Know About Specialized Care for Stroke Survivors

How Nursing Homes Address Dietary Restrictions for Residents

How Long-Term Care Provides Stability and Comfort for Aging Adults

How to Make the Most of Physical Therapy in Short-Term Rehabilitation

How Speech Therapy Can Improve Cognitive and Language Skills in Seniors

How to Plan a Smooth Move to a Nursing Facility

How Nursing Homes Promote Independence Among Residents

How Nursing Homes Adapt to Cultural and Religious Needs

How Long-Term Care Facilities Ensure Safety and Security for Residents

How Long-Term Care Facilities Ensure Safety and Security for Residents

How to Find a Trustworthy Respite Care Provider

How to Encourage Hobbies That Support Recovery

Why Consistency is Key in Rehabilitation Exercises

Creating a Care Plan for Post-Surgical Wound Management

Benefits of Group Therapy in Rehabilitation Facilities

How to Develop a Positive Mindset for Rehabilitation Success

How to Build Confidence After Surgery or Injury

How to Manage Post-Traumatic Stress After an Injury

Managing Chronic Illness with Short-Term Rehabilitation

Creating a Daily Recovery Checklist for Patients

Creating a Daily Recovery Checklist for Patients

How to Use Adaptive Equipment for Daily Living Tasks

How to Regain Hand Strength After Surgery or Injury

How to Improve Communication Skills Through Speech Therapy

How to Adapt Your Home for Safe Mobility After Rehabilitation

How to Improve Posture for Better Recovery Outcomes

How to Create a Safe Sleeping Environment for Recovery

How to Manage Emotional Burnout During Recovery

How to Safely Perform Daily Living Activities After Surgery

How to Prevent Bedsores in Long-Term Rehabilitation

How to Maintain Positive Relationships During Recovery

How to Adapt to Lifestyle Changes After Surgery

Creating a Structured Routine for Rehabilitation Success

Creating a Meal Plan for Post-Rehabilitation Nutrition

How to Encourage Positivity in a Loved One’s Recovery Journey

Tips for Managing Weight During the Rehabilitation Process

How to Cope with Long-Term Pain After Surgery

The Role of Peer Support Groups in Recovery

How to Manage Side Effects of Pain Medications

The Role of Cognitive Behavioral Therapy in Rehabilitation

The Role of Cognitive Behavioral Therapy in Rehabilitation

How to Overcome Isolation During Rehabilitation

How to Manage Chronic Pain Without Medication

Strategies for Enhancing Cognitive Skills During Recovery

The Role of Caregivers in Supporting Rehabilitation Patients

How Art and Music Therapy Enhance Rehabilitation Outcomes

How to Manage Joint Pain in Rehabilitation

How to Avoid Common Setbacks in Short-Term Rehabilitation

How to Handle Stress During the Rehabilitation Process

How to Identify Signs of Depression During Recovery

How to Manage Blood Pressure During Rehabilitation

The Benefits of Holistic Approaches in Rehabilitation

How to Help Seniors Transition from Rehabilitation to Home

Coping with Muscle Stiffness During Rehabilitation

How to Strengthen Weak Muscles After Surgery

How to Manage Fatigue During Physical Therapy

How to Build Core Strength in Rehabilitation

How to Develop Coping Strategies for Physical Limitations

How to Develop a Meditation Routine for Stress Relief

How to Develop Better Sleeping Habits During Recovery

Creating a Positive Mindset for Recovery

The Role of Recreational Therapy in Rehabilitation Centers

Managing Depression During Short-Term Rehabilitation

Coping with Limited Mobility During Short-Term Rehabilitation

How to Build a Strong Support System During Rehabilitation

The Benefits of Music Therapy in Rehabilitation

How to Develop Patience During the Recovery Process

How to Manage Energy Levels During Recovery

The Importance of Goal Setting in Rehabilitation

How to Build Emotional Resilience During Recovery

The Role of Acupuncture in Rehabilitation Care

How to Stay Connected with Friends During Recovery

The Role of Chiropractic Care in Rehabilitation

How to Develop Fine Motor Skills During Recovery

How to Develop Time Management Skills in Recovery

The Role of Skilled Nursing in Long-Term Care

The Benefits of Life Story Work for Seniors in Long-Term Care

How Nursing Homes Support Seniors After Surgery

The Role of Preventive Care in Long-Term Care Facilities

The Benefits of Skilled Nursing Facilities for Seniors

The Benefits of Occupational Therapy for Seniors in Long-Term Care

How to Choose the Right Short-Term Rehabilitation Facility

How to Create a Comfortable Therapy Environment for Seniors

How to Plan for Future Long-Term Care Needs

How Short-Term Rehab Can Improve Quality of Life for Seniors

The Role of Occupational Therapy in Short-Term Rehabilitation

How to Advocate for Your Loved One in a Nursing Home

How Nursing Homes Coordinate with Hospitals for Seamless Care

The Advantages of Short-Term Rehabilitation in Nursing Homes

How Physical Therapy Enhances Mobility in Long-Term Care Residents

The Importance of Specialized Care for Chronic Conditions

How Recreational Therapy Supports Emotional Well-Being in Long-Term Care

Understanding the Different Therapies Offered in Short-Term Rehabilitation

The Role of Peer Support Groups in Senior Care Facilities

The Connection Between Mental Health and Senior Care

The Importance of Consistency in Therapy for Long-Term Care Residents

What to Expect During a Nursing Home Admission Process

What to Expect from a Respite Care Stay in a Skilled Nursing Facility

How to Maximize the Benefits of Short-Term Rehabilitation Therapy

The Benefits of Short-Term Respite Care for Seniors

The Role of Care Coordination in Managing Multiple Therapies

How to Identify the Best Short-Term Rehabilitation Facility for Your Needs

The Role of Advanced Medical Services in Short-Term Rehabilitation

The Difference Between Outpatient and Inpatient Short-Term Rehabilitation

Top Questions to Ask When Touring a Nursing Facility

How Nursing Homes Manage Chronic Pain for Seniors

The Importance of Hydration in Senior Care

The Importance of Personalized Care Plans in Respite Care

How to Transition from Hospital to Short-Term Rehabilitation Seamlessly

How to Know When a Loved One Needs Respite Care Services

How to Ensure Continuity of Care in a Long-Term Care Setting

The Benefits of On-Site Specialists in Long-Term Care Facilities

The Benefits of On-Site Specialists in Long-Term Care Facilities

How to Prevent Rehospitalization After a Short-Term Rehab Stay

The Role of Physicians in a Long-Term Care Setting

How Aqua Therapy Benefits Seniors in Rehabilitation and Long-Term Care

The Importance of Nutrition in Short-Term Rehabilitation

How Short-Term Rehabilitation Prepares Patients for a Safe Return Home

How Personalized Care Plans Enhance Medical Services in Long-Term Care

The Importance of 24/7 Nursing Care in Long-Term Care Facilities

The Importance of Palliative Care in Long-Term Care Facilities

The Benefits of Professional Nursing Support in Respite Care

How to Support a Loved One in Short-Term Rehabilitation

How Respite Care Can Help Families Navigate Caregiver Fatigue

How to Prepare for a Short-Term Rehabilitation Stay

How Therapy Supports Aging Adults with Neurological Disorders

How Short-Term Rehabilitation Supports Recovery After Joint Replacement

How Short-Term Rehabilitation Supports Recovery After Joint Replacement

How Respite Care Supports Family Caregivers and Their Loved Ones

How Long-Term Care Facilities Provide Individualized Therapy Plans

How Family Involvement Supports Short-Term Rehabilitation Success

The Benefits of Having Access to Medical Services During Respite Care

How Skilled Nursing Supports Recovery in Short-Term Rehab

How Therapy Encourages a Faster Return to Daily Activities After Injury

What to Expect from Medical Services in a Skilled Nursing Facility

The Importance of Occupational Therapy in Daily Living Activities for Seniors

How Pain Management Enhances Recovery in Short-Term Rehab

How Sensory Stimulation Therapy Supports Seniors with Dementia

How Speech Therapy Supports Communication and Swallowing in Long-Term Care

The Benefits of Short-Term Respite Care for Seniors and Families

How to Maximize Progress During a Short-Term Rehabilitation Stay

The Connection Between Physical and Mental Health in Long-Term Care Therapies

How Pain Management Therapy Enhances Comfort for Long-Term Care Residents

How to Advocate for High-Quality Medical Services in Long-Term Care

How Respiratory Therapy Helps Manage Breathing Conditions in Long-Term Care

Common Conditions Treated in Short-Term Rehabilitation Programs

The Benefits of Short-Term Rehabilitation for Seniors

How to Incorporate Therapy into Daily Life in a Long-Term Care Facility

How to Choose the Right Therapy Program for a Senior’s Needs

The Importance of Personalized Care in Short-Term Rehabilitation

What to Do if You Suspect Neglect in a Nursing Home

How Nursing Homes Offer Support for Grieving Families

How Nursing Homes Utilize Telemedicine for Resident Care

How Alternative Therapies Support Wellness in Long-Term Care Facilities

How Nursing Homes Support Seniors with Respiratory Conditions

How Nursing Homes Promote Mental Wellness for Seniors

The Benefits of Regular Family Visits for Nursing Home Residents

How to Recognize the Signs That a Loved One Needs Long-Term Care

How Mental Health Support Helps in Short-Term Rehabilitation

How Nursing Homes Provide Emergency Medical Services

How Nursing Homes Provide Support for Parkinson’s Patients

Tips for Communicating Effectively with Nursing Home Staff

How to Choose the Right Nursing Home for Your Loved One

The Importance of Social Activities in Senior Care Homes

Why Family Involvement Matters in Long-Term Senior Care

Tips for Helping Seniors Adjust to Life in a Nursing Facility

The Role of Speech Therapy in Treating Swallowing Disorders

How Nursing Homes Handle End-of-Life Care with Dignity

How to Maintain Progress After Completing Short-Term Rehabilitation

How to Identify Warning Signs of Illness in Elderly Residents

How to Identify Warning Signs of Illness in Elderly Residents

How Personalized Therapy Plans Enhance Short-Term Rehabilitation

The Importance of Mental Health Services in Long-Term Care

How Short-Term Rehabilitation Supports Recovery from Orthopedic Injuries

The Importance of a Support Network in Short-Term Rehabilitation

How to Handle Emotional Challenges During Short-Term Rehabilitation

Why Short-Term Rehabilitation is a Stepping Stone to Long-Term Care

How to Stay Engaged and Active in a Long-Term Care Setting

The Role of Dietitians in Short-Term Rehabilitation

The Role of Recreational Therapy in Short-Term Rehabilitation

How Personalized Care Enhances Recovery in Short-Term Rehab

How to Avoid Complications During Short-Term Rehabilitation

The Benefits of Group Therapy in Short-Term Rehabilitation

The Benefits of Short-Term Rehabilitation for Faster Recovery

The Role of Hospice Care in Long-Term Care Facilities

The Role of Physical Therapy in Long-Term Care for Maintaining Mobility

How to Transition from Short-Term Rehabilitation to Home Care

How Physical Therapy Improves Strength and Mobility in Short-Term Rehab

How Short-Term Rehab Helps Prevent Hospital Readmissions

How Respite Care Helps Seniors Transition to Long-Term Care

How Caregivers Can Support a Patient’s Short-Term Rehabilitation Journey

The Benefits of Palliative Care in Long-Term Care Facilities

How Personalized Care Plans Improve Short-Term Rehabilitation Outcomes

How Long-Term Care Facilities Support Family Involvement

Understanding Memory Care Services in Long-Term Care

How Short-Term Rehabilitation Prepares Patients for Independent Living

How Support Groups Help Families Navigate Long-Term Care Decisions

Why Short-Term Rehabilitation is Essential After Joint Replacement Surgery

The Role of Nutrition in Long-Term Care for Healthy Aging

Managing Pain Effectively in Short-Term Rehabilitation

How to Plan Financially for Long-Term Care Services

How Social Activities Improve Mental Well-Being in Long-Term Care

How Personalized Long-Term Care Plans Improve Quality of Life

What to Expect During a Short-Term Rehabilitation Stay

Speech Therapy in Short-Term Rehabilitation: Why It Matters

The Role of Medical Supervision in Respite Care Programs

How Short-Term Rehab Helps Patients Transition Back Home Successfully

The Role of Therapy Dogs in Short-Term Rehabilitation Recovery

How to Manage Medications During Short-Term Rehabilitation

How Short-Term Rehab Helps Patients Regain Independence

How Medical Services Support Chronic Disease Management in Long-Term Care

The Importance of Advance Directives in Long-Term Care

The Role of Therapy Dogs in Nursing Homes

How Nursing Homes Address Sleep Challenges in Seniors

Nutrition and Dining Services in Nursing Homes

How Nursing Homes Enhance Residents’ Quality of Life

The Impact of Cognitive Therapy on Residents with Dementia

The Importance of Infection Control in Senior Care Facilities

How Nursing Homes Support Families of Residents

The Benefits of 24/7 On-Site Medical Care in Nursing Homes

How to Transition Between Skilled Nursing and Home Care

How Nursing Facilities Ensure the Safety of Residents with Mobility Issues

Myths About Nursing Homes: What Families Need to Know

Signs It’s Time to Transition to a Nursing Home

How Nursing Facilities Incorporate Technology into Therapy Programs

How to Build Strong Relationships with Nursing Home Staff

The Benefits of Intergenerational Programs in Senior Care

How Nursing Homes Manage Pain for Their Residents

How to Encourage Social Interaction Among Seniors in Care

The Role of Volunteer Programs in Nursing Facilities

The Role of Physical Therapy in Nursing Homes

How Nursing Homes Address the Emotional Needs of Seniors

What Families Should Know About Caregiver Ratios in Nursing Homes

The Benefits of Pet Therapy in Senior Living Communities

How to Recognize Quality Care in a Nursing Facility

The Transition from Hospital to Skilled Nursing Care

How Nursing Homes Incorporate Residents’ Personal Preferences

The Impact of Group Activities on Senior Well-Being

Arthritis Knee Support

Assisted Living Facility Statistics

How To Care For Aging Parents When You Can't Be There?

Occupational Therapy Games For Elderly

Nursing Home Readmission Rates Statistics

Do Nursing Homes Provide Hospice Care?

Benefits Of Pet Ownership For The Elderly

Stages Of Frontotemporal Dementia

Senior Education Programs

Nursing Home Neglect Statistics

Memory Care Facility Statistics

Homestead Hospice And Palliative Care

What Is Cardiac Care?

Woodworking And Crafts For Retirees

Nursing Home Facilities Near Me

Healthy Aging Workshops

Nursing Home Cost Statistics

Affordable Senior Living Near Me

Bariatric Care Facilities

Cooking Demonstrations For The Elderly

Art Galleries And Museum Visits

Healthcare For Seniors Statistics

Knee Pain Over 70 Years Old Treatment

Benefits Of Yoga For Seniors

What Services Are Available For The Elderly?

What Causes Knee Pain In Old Age?

Best Nursing Homes Near Me

Technology For Seniors

Free Government Programs For Seniors

Senior Health Outcomes Statistics

Day Trips And Excursions For Seniors

Activities For Seniors With Limited Mobility

What Is Outpatient Rehab?

Cost Of Memory Care Facilities Near Me

Drug Addiction In Seniors

Financial Management For Elderly

Home Healthcare Statistics

Virtual Support Groups For Seniors

Free Services For Seniors

Virtual Support Groups For Seniors

Tai Chi And Yoga For Older Adults

Nursing Home Physical Therapy Utilization Statistics

How Much Does Outpatient Rehab Cost?

Rehabilitation Facility Statistics

Nursing Home Resident Demographics Statistics

How To Prevent Seniors From Falling?

How To Treat Alcoholism In The Elderly?

Medicare Nursing Home Payment Statistics

Best Nursing Homes For Dementia Near Me

Seniors Addicted To Phone

Substance Abuse Among Seniors

Seasonal Celebrations For Retirees

Aging Population Statistics

Assistive Devices For The Visually Impaired

Wine Tasting Events For Retirees

Government Programs For Seniors Home Repairs

Retirement Community Amenities

Active Adult Communities

Senior Living Statistics

How To Deal With Aging Parent With Memory Issues?

Why Seniors Want To Stay In Their Homes?

Palliative Care Statistics

Senior Care Health & Rehabilitation Center

Elderly Care Resources

Nursing Home Mortality Rates Statistics

7 Stages Of Dementia Before Death

Medicare Coverage Options

Exercise Equipment For Seniors

Senior Care Facility Statistics

Games For Seniors With Dementia

Nursing Home Emergency Room Transfer Statistics

Elderly Care Statistics

Alzheimer's Care Statistics

High Blood Pressure In Elderly

What Does A Speech Therapist Do For Elderly?

Qualifications For Respite Care

Nursing Home Discharge Rates Statistics

Nursing Home Regulatory Compliance Statistics

Nursing Home Admission Rates Statistics

Average Length Of Stay In Nursing Homes Statistics

Nursing Home Medication Error Statistics

Home Health Care Agencies

Elderly Population Demographics Statistics

How To Prevent Knee Pain In Old Age?

Elder Law Considerations

Early Signs Of Alzheimer's Are In The Eye

Elderly Living Alone Problems

Average Cost Of Respite Care

Theater And Musical Performances For Elderly

Knitting And Crochet Groups For The Elderly

Nursing Homes With Hospice Care Near Me

More Than a Thousand Nursing Homes Reached Infection

What Causes Falls in the Elderly? How Can I Prevent a Fall?

Heart Healthy Recipes & Foods for Seniors

The Best Recumbent Bikes for Seniors

How Do You Eat Heart-Healthy on a Budget?

Tips for Dealing with Stubborn Aging Parents

What Can I Do About My Elderly Parent's Anxiety?

Falls in Older Adults

The Benefits of Exercise Bicycles for Senior Wellness

Incredibly Heart-Healthy Foods

Mental Health Resources For The Elderly

Early Signs Of Alzheimer's In 50s

End-Of-Life Care Statistics

Activities For Blind Seniors With Dementia

Heart Health For Seniors

Caring For Elderly Parents

How Long Does Stage 7 Dementia Last?

Dementia Care Statistics

Medicaid Eligibility Criteria

Government Assistance For Seniors With Low-Income

Benefits Of Pet Therapy For Seniors

Is Arthritis Avoidable?

Nursing Home Dementia Care Statistics

Senior Employment Resources

Dementia Support Services

Best Pain Medication For Elderly Patients

What Is Senior Care Services?

Senior Housing Subsidies

What Is Heart Failure In The Elderly?

Leisure Activities For Retirees

Hospice Care Statistics

Geriatric Care Statistics

Dual Diagnosis In Older Adults

Residential Care Facility Statistics

The Complete Guide to Senior Living Options

What to Expect When Starting Hospice Care at Home

Hospice Care While Living in a Nursing Home

Traditions Health: Hospice & Palliative

What Does In-Home Hospice Care Provide?

Homestead Hospice & Palliative Care

Different Types of Elderly Care Living Options

Do Nursing Homes Provide Hospice Care?

Where Is Hospice Care Provided and How Is It Paid For?

Why Hospice in the Nursing Home?

Affordable Housing Options For Retirees

How To Deal With Elderly Parents Anxiety?

Mindfulness And Meditation For Seniors

Heart-Healthy Foods For Seniors

Assisted Living Benefits

Residential Care Homes Near Me

Memory Care Facilities Near Me That Accept Medicare

Travel Options For Seniors

Memory Care Facilities Near Me

Activities For Seniors Near Me

Substance Use Disorder In Older Adults

How To Prevent Falls At Home For Elderly?

Senior Pharmacy Services

Assisted Living For Autistic Adults Near Me

Government Grants For Elderly Care

Lifelong Learning Opportunities

Skilled Nursing Facility Statistics

Fishing And Boating Excursions For Seniors

How Many Hours Of Respite Care Are You Allowed?

Social Media Tutorials For Seniors

Does Speech Therapy Help Alzheimer's?

Dual Diagnosis in Older Adults

Prescription Drug Misuse Among Older Adults

Alcoholism in the Elderly

Treatment for Substance Abuse in Older Adults

Overcoming the Dangers of the Elderly Living Alone

Living Alone with Dementia

Brain Games & Memory Exercises for Seniors

Activities to Enjoy if Someone Has Alzheimer's or Dementia

NHA Turnover and Nursing Home Financial Performance

Nursing Home Affiliated Entity Performance Measures

Addiction Rehab for Seniors & Elderly Adults

Nursing Home Care Statistics 2024

Engaging Nursing Home Residents with Dementia in Activities

Nurse Staffing Estimates in US Nursing Homes

Living Alone with Dementia: Lack of Awareness

Nursing Home Quality and Financial Performance

The Quality of Care in Nursing Homes

Nursing Home Staffing Levels

Meaningful Activities for Dementia Patients

Staffing Instability and Quality of Nursing Home Care

The National Imperative to Improve Nursing Home Quality

Organizational Culture and High Medicaid Nursing Homes

Alcohol & Aging: Impacts of Alcohol Abuse on the Elderly

Prescription Drug Abuse in the Elderly

Nursing Home Staffing Data

Determinants of Successful Nursing Home Accreditation

Caregiver Statistics

Who Are Family Caregivers?

The Important Role of Occupational Therapy in Aged Care

Cost Of Drug And Alcohol Rehab

Older Adult Fall Statistics and Facts

Benefits of Living in a Golf Course Community

Retirement Hot Spots for Golfers

Best Online Resources for Older Adults

Understanding Senior Companion Care

Elderly Companion Care

Hospice Foundation of America

Personal Hygiene: Caregiver Tips for At-Home Hospice Patients

How To Care For A Hospice Patient as a Caretaker

Hospice Care in an Assisted Living or Skilled Nursing Facility

Can you Receive Hospice Care in a Nursing Home?

Resources for Aging Adults and Their Families

Hospice Care in the Nursing Home

What Senior Care Options are Available for the Elderly?

Determinants of Successful Nursing Home Accreditation

Senior Care: Know Your Options

Nursing Home Falls Cause Injury & Death

Benefits of Occupational Therapy for Elderly

Companion Care for Seniors

Different Alternatives to Nursing Homes for the Elderly

Behavioral Health Care for Seniors

The Effect of Nursing Home Quality on Patient Outcome

Drug Rehab Success Rates and Statistics

Palliative Care Facts and Stats

The Importance Of Home Safety

Best Safety Devices for Seniors

Household Safety Checklist for Senior Citizens

What Is the Best Type of Yoga for Seniors?

Foods that are Good for your Kidneys

Tips to Relieve Stress of Caring for Elderly Parents

Hearing Aid: How to Choose the Right One

The Importance of Maintaining a Safe Home & Yard

How Many People Need Palliative Care?

Home Safety for Older Adults

An Aging-in-Place Strategy for the Next Generation

How Do Seniors Pay for Assisted Living?

What is Personal Home Care?

Caregiver Stress and Burnout

Most Recommended Forms Of Yoga For Seniors

The Best Hearing Aids for Seniors

Learn the Six Steps to Aging In Place Gracefully

Avoiding Burnout when Caring for Elderly Parents

Nursing Home Mortality Rates and Statistics

Occupancy is On the Rise in Nursing Homes

How to Pay for Assisted Living: A Comprehensive Guide

How to Deal With Aging Parents' Difficult Behaviors

Dealing with Aging Parents

Seven Signs Elderly Parents Need More Support at Home

Factors to Consider Before Moving Your Elderly Parents In

Tips on How to Cope with Parents Getting Older

Resources for Adult Children Caring For Aging Parents

This Is What Happened When My Parents Moved In

Arthritis Awareness Month

Signs Your Elderly Parent Needs Help

Take Extremely Good Care of Your Elderly Parents

The Role of the Speech Pathologist in Aged Care

The Benefits of Cooking Classes for Seniors

Trusted In Home Care for Seniors & Quality Senior

Benefits of Telemedicine for Seniors

Advantages & Benefits of Home Care for Seniors

Fun Classes for Senior Citizens to Take

Telemedicine in the Primary Care of Older Adults

What is End-Stage Dementia?

Cooking Activity Ideas for Seniors & the Elderly

Late-Stage Dementia and End-of-Life Care

Volunteer Abroad Opportunities for Seniors and Retirees

Health Benefits of Music Therapy for Older Adults

Understanding Assisted Living Levels of Care

Guidelines for Admission to the Acute Inpatient

Senior Care Services & Assisted Living Levels of Care

Benefits of Inpatient Rehabilitation

Amazing Benefits Of Music Therapy for Seniors

Inpatient Vs. Outpatient Rehab

What is Inpatient Rehab?

Are There Different Levels of Assisted Living?

Why Seniors Should Join a Knitting Club

Teaching Older Adults to Knit and Crochet

A Beginner's Guide to Power of Attorney for Elderly Parents

Long Term Care Planning

What to Expect When Starting Hospice Care at Home

Home Health Aide Do's and Don'ts

What Are Home Health Aides Not Allowed To Do

Hospice Home Care What to Expect

Late Stage and End-of-Life Care

What End of Life Care Involves

Healthful Foods for Fighting Kidney Disease

Depression in Elderly Parents: How to Help

Moving a Person with Dementia into a Caregiver's Home

How Long do People Live in Hospice Care?

Eating Right for Chronic Kidney Disease

The Hospice Care in Nursing Homes Final Rule

The Role of Hospice Care in the Nursing Home Setting

Seven Tips for a Successful Move to Dementia Care

Ways to Help Your Elderly Parents Deal With Depression

Does Hospice Cover 24-Hour Care at Home?

Golden Years Gourmet: Cooking Classes for Seniors

The Best Phones for Seniors in 2024

Nursing Home Care Compare

Home Health Aids vs. Personal Care Aides

Top 5 Benefits of Cooking Classes for the Elderly

Care in the Last Stages of Alzheimer's Disease

What Is a Home Health Aide?

Memory Care Facilities That Accept Medicaid and Medicare

The Best Cell Phones for Older Adults

Dementia and End of Life Planning

Exercise Bikes For Seniors

What is a Rehabilitation Center for the Elderly?

What to Know About Senior Centers

Why Senior Outings Are Important?

The Power of Creative Writing Exercises for Senior Minds

Wordfind: Cultural Activities for Seniors

Popular Senior Center Book Club Books

Birdwatching Helps Older Adults Reconnect with Nature

What Services Do Senior Centers Provide?

Top 5 Benefits of Senior Book Clubs

Does an Older Adult in Your Life Need Help?

Enriching Assisted Living and Nursing Home Activities

High Blood Pressure and Older Adults

Tips to Avoid Heatstroke and Heat Exhaustion

What Are the Causes of Hypertension in Older Adults?

Preventing Heat-Related Illness

Assisted Living Activities and Calendar

Caregiving: Taking Care of Older Adults

Signs Your Aging Parent Might Need Help

Heatstroke - Symptoms and Causes

What Is Long-Term Care?

Hospice Care in the Nursing Home

What Are the Four Levels of Hospice Care?

Home Health Aide Duties: What Does an HHA Do?

How Many Hours Can a Home Health Aide Work?

How to Become a Paid Caregiver for Elderly Parents

Pros And Cons Of Nutritional Supplement Drinks

How Long is the Average Hospice Stay?

In-Depth Guide on Taking Care of Elderly Parents

Nourishing and supplementary drinks

Can I Afford a CCRC? Here's What You Need To Know

Guardianship-Acting for the Disabled Adult

Helpful Online Resources for Seniors

Are Continuing Care Retirement Communities a Good Idea?

Does Medicare Cover Palliative Care?

Helping an Elder Make a Power of Attorney

Medicare and End-of Life Care: What to Know About Coverage

Guardianship and Conservatorship of Incapacitated Persons

How to Get Power of Attorney for an Elderly Parent

Online Resources for Senior Health

Speech Therapy for People with Alzheimer's

Occupational Therapy Sensory Processing Disorder

Speech Therapy and Alzheimer's Disease

Healthy Weight Gain for Older Adults

The Benefits of a Senior Rehabilitation Center

Treating Sensory Processing Issues

What to Look for When You Need Senior Rehabilitation

Top Foods To Help Seniors Gain Weight

What to Expect When Your Loved One Is Dying

End-of-Life Stages Timeline for Hospice Patients

Different Types of Trusts for Seniors

Estate Planning for Seniors: What to Know

Hospice Care Vs. A Nursing Home

Tips on How to Take Care of the Elderly in Your Home

Mental Health Of Older Adults

How Long Does The Average Hospice Patient Live?

What Drugs Are Used in End-of-Life Care?

What to Do When You Can't Care for Elderly?

Older Adults and Mental Health

End-of-Life Care: Managing Common Symptoms

How Long Can You Be On Hospice?

End-of-Life Care and Hospice Costs

Hospice vs. Nursing Home: What is the Difference?

Does Medicare Cover Memory Care Facilities?

Can I Take Care of Elderly in My Home?

Adult Disability Homes (ADHs)

Long-Term Care Facilities: Types and Costs

Residential Care Homes for Disabled Adults

Hospice Care at Home Cost: What You'll Pay

Is Memory Care Covered by Medicare?

Types of Facilities - Long-Term Care - Senior Health

Ageing and Long-Term Care

Understanding Long-Term Care for Older Adults

Long-Term Care Facilities

Understanding Residential Care Homes for Disabled Adults

What is Memory Care?

What Is Respite Care?

Are Nursing Homes Covered by Long-Term Care Insurance?

What Does Independent Living Mean in the Senior Living?

Personal Transportation for Seniors

Best Home Remodels For Aging In Place

Eldercare Resources

Top 10 Ways to Prepare for Retirement

The Best Mobility Devices for Seniors in Every Environment

Independent Living for Seniors

Understanding Long-Term Care Insurance

Services for Older Adults Living at Home

What is Senior In-Home Care? Home Health Care Guide

Retirement Home vs. Long Term Care

3 Types of Long Term Senior Living

5 Retirement Planning Steps To Take

What is a Memory Care Facility?

The Ultimate List of Aging in Place Home Modifications

Health Benefits of Pet Therapy in Seniors

The Benefits of Pet Therapy for Senior Caregiving

What Are the Options for Senior Transportation?

Does Insurance Cover Nursing Homes?

What Is Retirement Planning?

8 Useful Mobility Aids for Seniors with Disabilities

What Is Pet Therapy for Seniors?

Transportation for Older Adults

What is the Specialized Dementia Care Program

Does Insurance Pay for Nursing Home?

Nursing Home vs. Memory Care: What's the Difference?

Benefits of Pet Therapy for Seniors

What is the Average Length of Stay for Rehab?

Unpacking Assisted Living

Why Do Seniors Want to Stay in Their Homes?

Palliative Care vs. Hospice: Which to Choose

How to Report a Home Health Aide?

What Is A Home Health Nurse?

How Long Can You Stay in Acute Rehab?

What is Home Nursing Care and What Does it Cover?

The Right Alzheimer's Care for Your Loved One

Difference Between Hospice and End-Of-Life Care

Taking Care of Elderly Parents Quotes

Top 10 Complaints from Home Care Clients

How to Get an Elderly Person into a Care Home

Your Guide To Luxury Senior Living

Aging in Place: Growing Older at Home

What Qualifies for Acute Rehab?

The Mental Health Benefits of Socializing for Seniors

How Much Does Inpatient Physical Rehab Cost?

What Is The Difference Between Acute And Subacute Rehab?

Inpatient Rehab Physical Therapy

Exercise Programs That Promote Senior Fitness

The Benefits of Socialization for Seniors in Senior Living

Total Body Strength Workout for Seniors

Healthy Eating Tips for Seniors

Best Wellness Programs for Seniors

Falls and Fractures in Older Adults: Causes and Prevention

What are Acute Care Rehab Facilities?

Home Safety Tips for Older Adults

Assisted Living Activity Calendar Ideas

Why Inpatient Rehabilitation

6 Smoothies & Shakes for Seniors

Supplement Drinks for Elderly: Dietitian Recommendations

What Is Acute Rehabilitation?

Top 5 Incredible Home Made Nutritional Drinks for Seniors

What Is a Continuing Care Retirement Community?

What Are Palliative Care and Hospice Care?

Twelve Self-Care Tips for Seniors

Dietary Supplements for Older Adults

The Importance of Nutrition For The Elderly

What is Palliative Care for the Elderly?

Nutritional Needs for the Elderly

The Best Nutrition Drinks for Adults and Seniors

Essential Vitamins and Minerals for Seniors

Providing Care and Comfort at the End of Life

What To Look For in a Senior Rehab Facility

Why Is Self-Care Important for Seniors?

Alzheimer's & Dementia Care Options

Help With in-Home Care for Someone With Alzheimer's

How To Find In-Home Care For Disabled Adults

What is Personal Care? | Helping Hands Home Care

Specialized Care Facilities - Senior Living

Top 10 Tips For Caring For Older Adults

How Many Skilled Nursing Facilities are in the U.S.?

Importance of Elderly Care Services

Specialized Care Facilities Differ From Nursing Homes

Best Special Care Units for Older Adults

Senior Rehab: Better Care Options After a Hospital Stay

What are the Benefits of a Senior Rehabilitation Center?

Differences Between Skilled Nursing Facilities and Hospitals

What Services Do Seniors Need Most?

Senior Continuing Care Communities

How Much Does a CCRC Cost?

How Continuing Care Retirement Communities Work

What is a Continuing Care Retirement Community?

The Top 10 Benefits of a Skilled Nursing Facility

Who Should Go to a Skilled Nursing Facility?

What is a Skilled Nursing Facility?

3 Main Benefits Of Continuing Care Retirement Community

Family Medical Care Center

Home Care for Disabled Adults

7 Benefits of In-Home Care for Older Adults

Home Care Services for Seniors: Aging in Place

Personal Care Needs of the Elderly

Caregiver Duties for Disabled Adults

A Guide to VA Nursing Homes

What Are the Types of Nursing Homes?

Hospital vs. Freestanding: Which setting is the best?

What is Urgent Care Medicine?

Requirements for Nursing Home Administrator Licensure

What is Data Privacy in Healthcare?

When Is It Time for a Nursing Home?

Kaiser Permanente and Senior Care Coverage

Nursing Home Employee Background Checks

Types of Services Offered at a Skilled Nursing Facility

Do VA Benefits Pay for a Nursing Home?

Skilled Nursing Facilities

Moving Into a Nursing Home: A Packing List

Benefits of a Free-Standing Treatment Center

Acute Rehabilitation vs. Skilled Nursing

Types of Skilled Nursing Care

Average Cost of Skilled Nursing Facilities in 2024

When Medicare Stops Covering Nursing Care

Inpatient Acute Rehabilitation Centers

Patient Confidentiality

What Kinds of Services Are Provided at Urgent Care?

Best Gift Ideas for Nursing Home Residents

How does a Patient Qualify for Skilled Nursing Care?

Veterans Eligibility for VA Nursing Home Care

6 Nursing Home Resident Necessities

What Qualifies a Person for a Nursing Home?

The Q Word Podcast: Emergency Nursing

How to Find In-Home Care Financial Assistance

What Is a Home Health Aide? A Career Guide

Levels of Healthcare

Types of Home Health Care Services

Differences Between Assisted Living and Nursing Homes

What Aged Care Homes Provide

What To Bring To A Skilled Nursing Facility

What Is A Home Care Grant

Does Medicare Pay for Nursing Homes?

What to Expect from Skilled Nursing

What is In-Home Care?

How Much Does Long-Term Care Insurance Cost?

Skilled Nursing Facility vs. Nursing Home

Skilled Nursing Facility Levels of Care

What to Expect When Working in a Nursing Home

Nursing Home Costs and Payment Options

Nursing Home Insurance

Nursing Home Requirements: Who's Eligible?

What Caregivers Should Know About Nursing Home Care

How Can I Pay for Nursing Home Care?

Understanding the Four Levels of Hospice Care

The Top Amenities Every Skilled Nursing Home Should Have

A Guide to Nursing Homes

Guidance for Elderly Individuals on Handling Disabilities

Contact us today and experience ”The Name in Healthcare”

Where compassion, well-being, and a welcoming community converge to redefine your healthcare journey. Welcome to Rosewood, where your family becomes our family.